Why is the CFEA still needed in the UK?

Why is the CFEA still needed in the UK?

A reminder of why we do what we do

Also in this series:

Here are some of the more interesting quotes I remember hearing the last several months in the investor/founder ecosystem about the model:

“Why do I need to talk to a Friends and Family Round VC if I can just call up my friend and he’ll give me $500,000 of pre-seed capital to start a business if I needed?” (founder)

“Why would I want to tack on extra debt? I only want to give up equity. Much less responsibility for me.” (founder)

“10K-20K? That’s way too little.” (investor)

“Aren’t you worried about your returns? Wouldn’t you get spurned by the best founders who can raise a pre-seed round within days?” (investor)

The interesting thing about a lot of these comments is that they are perfectly valid… when viewing from the perspective of one type of founder or one type of investor or even one type of LP. Unfortunately, a startup ecosystem consists of many types of founders… and many types of investors… and many types of LPs who fund many types of VCs. When viewing from the totality of what exists out there, one can observe the startup ecosystem in the UK (and the EU as well) and see that large funding gaps for talented founders still exist in the market. And considering that the world is projected to head into a recession, and we can see that more than ever, we need alternative capital models to fund different kinds of startups.

Most founders are not suited for pure equity.

Pure equity looks like a great deal to an average entrepreneur because on the surface, it seems to have the lowest level of responsibility and “equity” seems like an abstract concept that won’t matter several years down the road. Except equity is not an abstract concept that matters years down the road, but dictates how most investors will want you to grow your business in order to satisfy their need for high returns. This “initial lack of responsibility” comes back around as a need to secure your investor’s need for returns, because the VC Power Law states that 9/10 investments will return 0-1x, meaning that one of them will need to return north of 20x in order to secure a roughly 3x MOIC over 10 investments. That means that in order for an angel investor/VC to invest in you using this arrangement, it has to look like a business that could potentially scale to 20x. Which means micro-SaaS, tea brands, and other types of businesses that have the potential to scale to appx. 7 figures in ARR don’t suit traditional equity models because while it may look like a success to the founder, it does not look like success to a traditional VC.

Pure equity is not great for funding friends and family round businesses, and thus those that don’t have rich friends and family kind of get the short end of the funding stick.

ASA/SeedFASTs aren’t great for funding idea stage (earlier than pre-seed) founders because at that early stage, the failure rate and economics behind these equity-only instruments cease to make as much sense from a returns standpoint. Without some sort of downside protection, particularly in Europe, it’s tough to convince angels and VCs to go in and be a “friends and family round” substitute. This leaves “actual friends and family” to have to come in and pick up the slack, but unfortunately those without access to wealthy friends and family get the short end of the funding stick. And that’s how talented founders from non-“classy” backgrounds continually get shafted in the investing world.

Other alternative capital options don’t adequately serve founders either.

Let’s look and see what other options exist in the UK/EU for founders that don’t want to turn to traditional VC:

Loans:

Generally only fund businesses/people with collateral (physical assets).

More suited to those who are attempting to start restaurants or small corner shops.

Require you to pay monthly no matter what the condition your business is in, and there’s limited ability to defer.

Eg: Virgin Startup Loan/British Business Bank

Borrow from £500 to £25K per co-founder (Virgin), or up to £25K total (British Business Bank)

Borrow over 1-5 years at a fixed interest rate of 6% p.a.

Revenue Based Financing

Eg: Uncapped

Non-dilutive funding from £100k to £10M

Minimum 6+ months of trading

Minimum £100K+ in monthly revenue

Grants

Eg: Innovate UK

Very low acceptance rate

Must have a clear game-changing idea -> new products/services

Must have realistic potential for global markets

Will not fund commercialisation activities

Must start by 1 October 2022 and end by 30 September 2025 (Innovate UK funding, not project)

If your project’s duration is 6 to 18 months it:

must have total eligible project costs between £100,000 and £500,000

can be single or collaborative

If your project’s duration is 19 to 36 months, it must:

have total eligible project costs between £100,000 and £2 million

be collaborative

Crowdfunding

Must be based in UK, EU, EEA (European Economic Area), Switzerland

Target raise should be over £50000

Extremely competitive

D2’S “HERO”

Venture Path”

D2 invests £500k at a pre-money of £4.5M and receives an option on 10% of the business.

The company receives a term sheet from a Series A venture fund and the HERO converts ahead of the round into a 10% shareholding.

At this point the HERO falls away and the equity issued by the conversion of the HERO is diluted by the new money coming into the business, exactly in the same way as a SAFE.

Efficient Growth:

After two years the rev share kicks; D2 earns a return and the founder is able to effectively buy back equity on the cheap.

After five years the rev share stops and shortly after the company raises a growth round. ¾ of the HERO has already been bought back via the rev share - the remaining 2.5% (¼ of 10%) converts into equity ahead of the round.

“Off Ramp:” (stable, revenue generating business)

Here the revenue share element of the HERO functions as an ‘off ramp’ The rev share means that the investor recovers part of their investment and redeploys it elsewhere in their portfolio.

The founder is then free to choose how to take their business forward without the pressure of an investor pushing for the company to artificially become something it’s not

Great option for those that are working on a larger pre-seed/seed business, but not at the friends and family round stage

So as one can observe, there are still not a bunch of great options at the friends and family round stage other than “Virgin Startup Loan” which forces you to pay no matter if you are doing well or doing poorly.

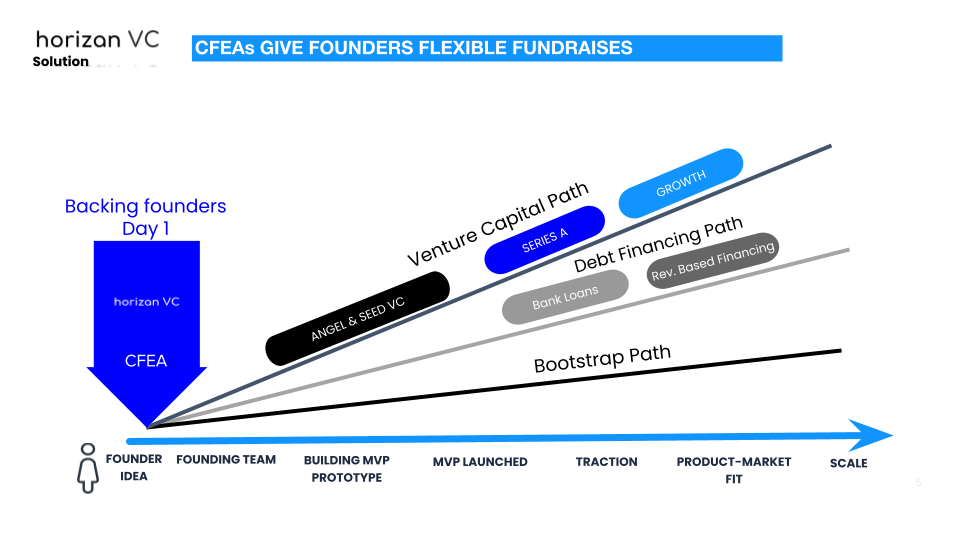

A CFEA model enables founders to flexibly build any type of business they’d want, with the fund still receiving returns.

For more detailed information about our terms, read here. In short though: CFEAs allow founders to choose whether they want to eventually build a stable revenue generating business, or something that is venture-backable, and we’ll get our returns either way.